FMP

Learn Financial Modeling: Discounted Cash Flow statement (DCF) Methodology

Sep 30, 2022 5:08 AM - Jack Dalton

Image credit: John Schnobrich

2. Build A Cash Flow Statement

The Discounted Cash Flow Analysis is a valuation methodology that measures the intrinsic value of a business. This is based on the present value of the company's future free cash flow.

You may have created a financial statement before that precedes the DCF analysis. However, you may be wondering why you're using a free cash flow build-up when you already have a cash flow model. The answer: Cash flow from operations does not include long-term capital expenditures or investment revenue and expense.

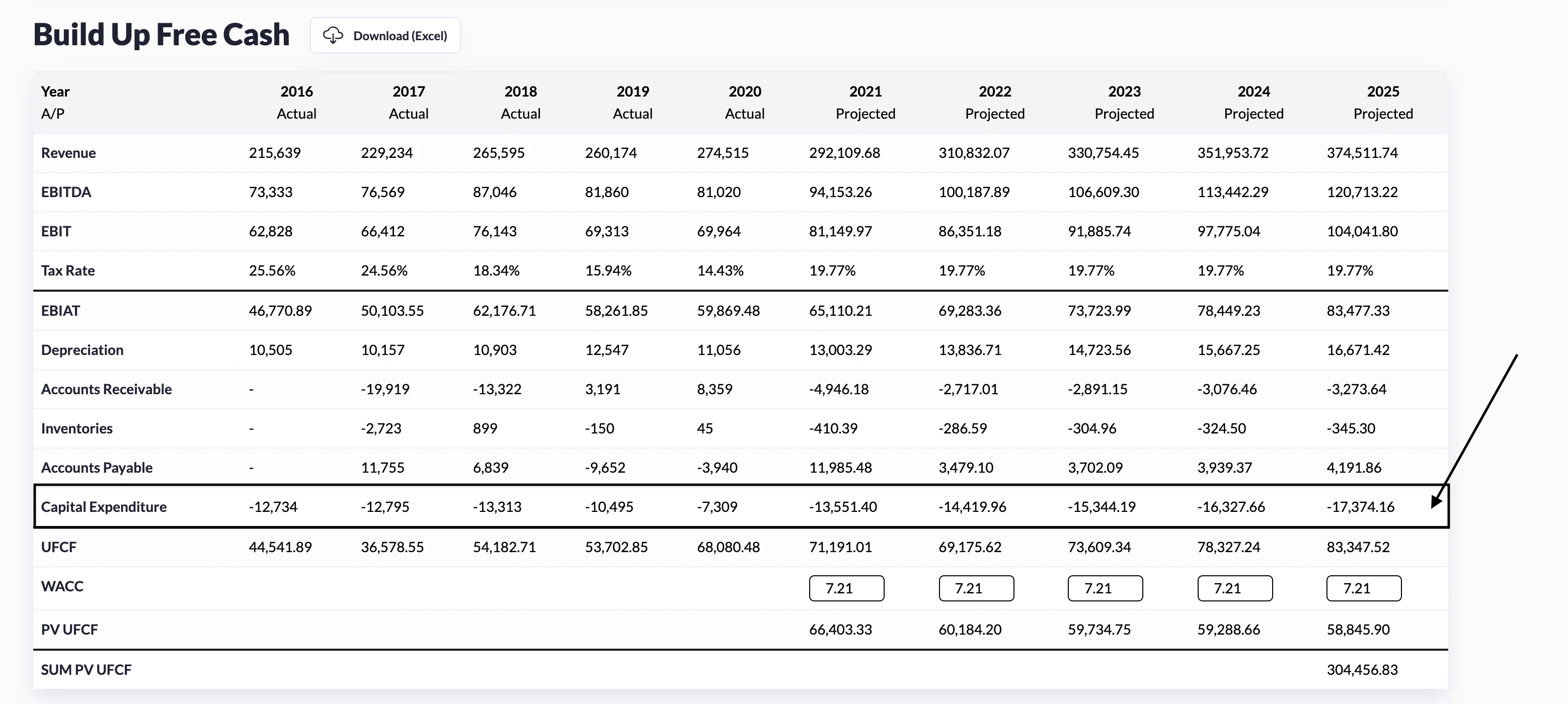

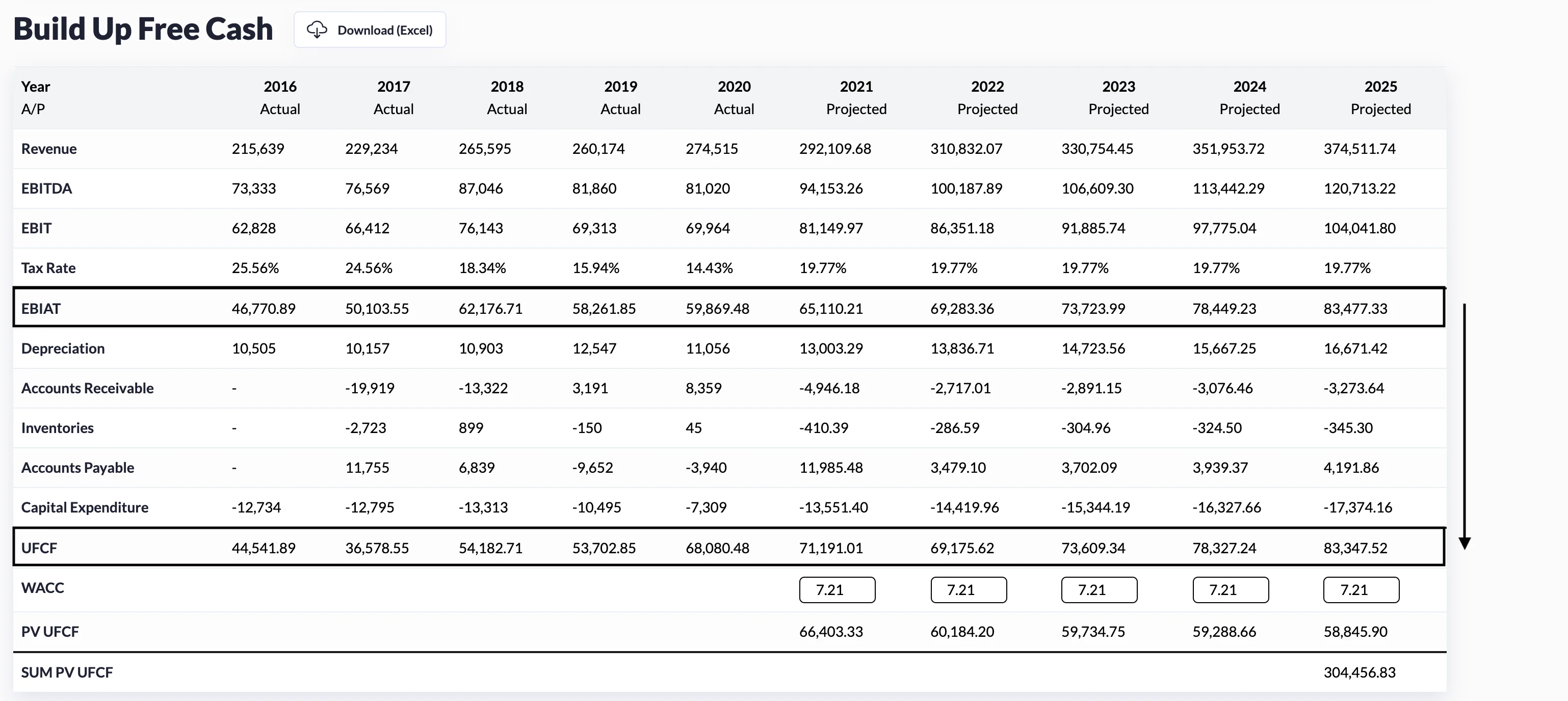

We know that free cash flow is operating profit minus the capital expenditure reinvestment and working capital changes. Cash flow from operations is missing a critical element which is capital expenditure. Thus, a cash flow build-up is needed as presented in the diagram.

The next thing that you are probably wondering is why we forecast for 5 years.

A great forecast includes operating results and resource requirements projections for the next 3-5 years. Moreover, established companies like Coca-Cola and Procter & Gamble still conduct five-year forecasts.

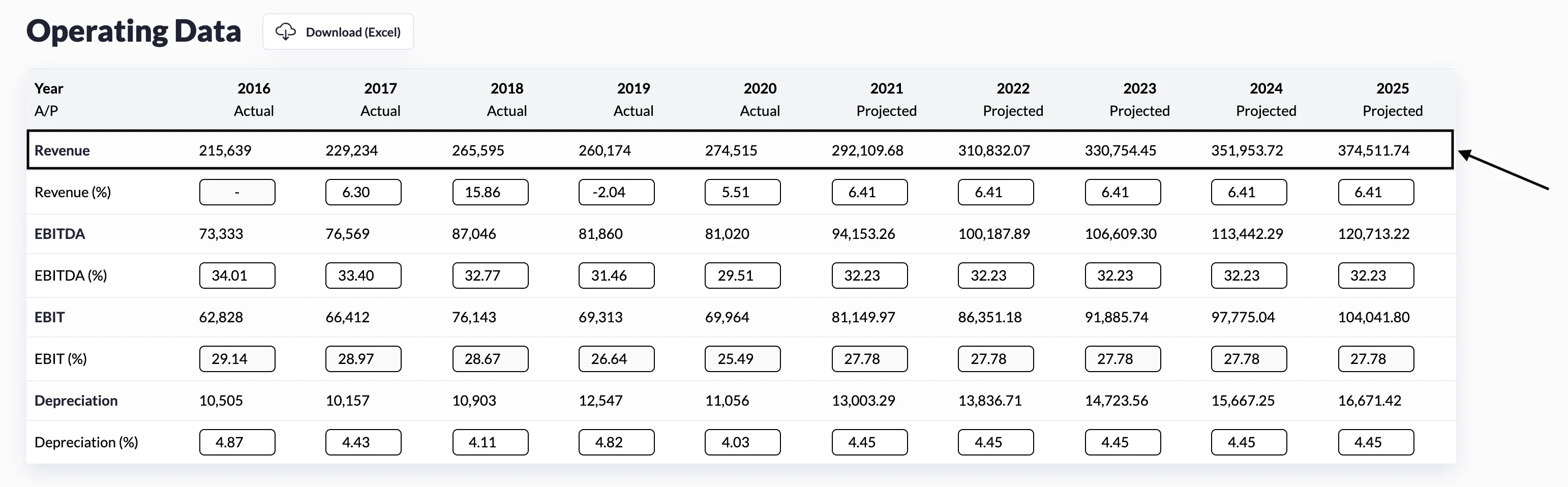

This is to gain a holistic overview about the firm's cash flow build-up. Now that we understand what this section entails, let's start building a discounted cash flow statement. We are going to reference revenues from our select operating data schedule.

The same will be done with EBITDA, EBIT, and Depreciation.

This is an unlevered free cash flow analysis. It is unlevered because it is before the debt is paid. Given that taxes are not optional we are going to focus on earnings before interest after taxes (EBIAT). We take earnings before interest and taxes (EBIT) and multiply that by 1 then subtract the tax rate to find the after-tax value of EBIAT.

Another word for EBIAT that you might hear is NOPAT (Net Operating Profit After Taxes). Net operating profit after tax (NOPAT) is a business's potential cash earnings if its capitalization were unleveraged. does not include tax savings from existing debt.

To calculate NOPAT, first, we need to deduct the EBIT with the adjustable tax amount. The formula for NOPAT is:

NOPAT=Operating Income × (1−Tax Rate)

where: Operating Income = Gross profits less operating expenses

To determine the company's EBIT, we need to subtract the cost of goods sold and operating expenses (selling, general, and administrative expenses) from the company's total revenue.

EBIT = Total revenue - Cost of goods sold - Operating expenses

Now, the company's tax rate is disclosed in its annual report. Following that, we calculate the tax-adjusted value by subtracting the tax rate from one, i.e. (1 - Tax rate).

Lastly, the formula for NOPAT is derived by multiplying the EBIT with the determined value. We need to make several adjustments to go from EBIAT to unlevered free cash flow (UFCF). Those adjustments include adding back non-cash expenses, taking out non-cash gains, and changes to working capital. We'll make our accrual adjustments and then subtract our reinvestment which leaves our capital expenditure.

Thus, the first step will be to add our non-cash expenses. In this case, it is simply depreciation and amortization (D&A). Next, we must determine the change in working capital. When building a cash flow statement, increasing the value of an asset is considered a use of cash. I understand how difficult it is to see why an increase in accounts receivable is a cash use, so I'll explain it from a different perspective.

We know that both cash versus accrual accounting revenues includes both sales made on credit as well as sales made with cash. In other words, if our credit sales increase, that will indeed increase revenue, but we know that we are not actually receiving the cash.

We will receive it in the future. If our accounts receivable increase, we must adjust our EBIAT to reflect only the actual cash that is received, which is cash sales. Therefore, an increase in accounts receivable will need to be deducted from EBIAT to reflect only the actual cash which is cash sales. Increases in accounts receivable must be deducted from EBIAT in order to accurately reflect only cash received.

One method is to subtract the previous year's accounts receivable from the first forecasted year If there was an increase in accounts receivable, you need to add a negative sign to that value; otherwise, you will not have the correct signage.

Since accounts payable is a liability, an increase in that represents a source of cash and would add it. Do the first forecasted period minus the previous period to determine the change.

Capital expenditures are an asset; an increase represents a use of cash.

Now, what we need to do is add EBIAT, D&A, and our working capital adjustments. Next, subtract the Capital Expenditures (CAPEX).

This gives us unlevered free cash flow for each period (UFCF). To calculate the present value of UFCF, we will divide the forecasted value by 1 then add the weighted average cost of capital (WACC) raised to the forecasted period.

We have built up our free cash flow for each forecasted period which is stage one. Now it's time to concentrate on stage two, which is the final value.

Remember that the WACC is still required to convert unlevered free cash flow (UFCF) to the present value of unlevered free cash flow (PV UFCF). We'll calculate it after we've determined the terminal value, which comes next. Go to terminal value.

Other Blogs

Sep 11, 2023 1:38 PM - Rajnish Katharotiya

P/E Ratios Using Normalized Earnings

Price to Earnings is one of the key metrics use to value companies using multiples. The P/E ratio and other multiples are relative valuation metrics and they cannot be looked at in isolation. One of the problems with the P/E metric is the fact that if we are in the peak of a business cycle, earni...

Sep 11, 2023 1:49 PM - Rajnish Katharotiya

What is Price To Earnings Ratio and How to Calculate it using Python

Price-to-Earnings ratio is a relative valuation tool. It is used by investors to find great companies at low prices. In this post, we will build a Python script to calculate Price Earnings Ratio for comparable companies. Photo by Skitterphoto on Pexels Price Earnings Ratio and Comparable Compa...

Oct 17, 2023 3:09 PM - Davit Kirakosyan

VMware Stock Drops 12% as China May Hold Up the Broadcom Acquisition

Shares of VMware (NYSE:VMW) witnessed a sharp drop of 12% intra-day today due to rising concerns about China's review of the company's significant sale deal to Broadcom. Consequently, Broadcom's shares also saw a dip of around 4%. Even though there aren’t any apparent problems with the proposed solu...